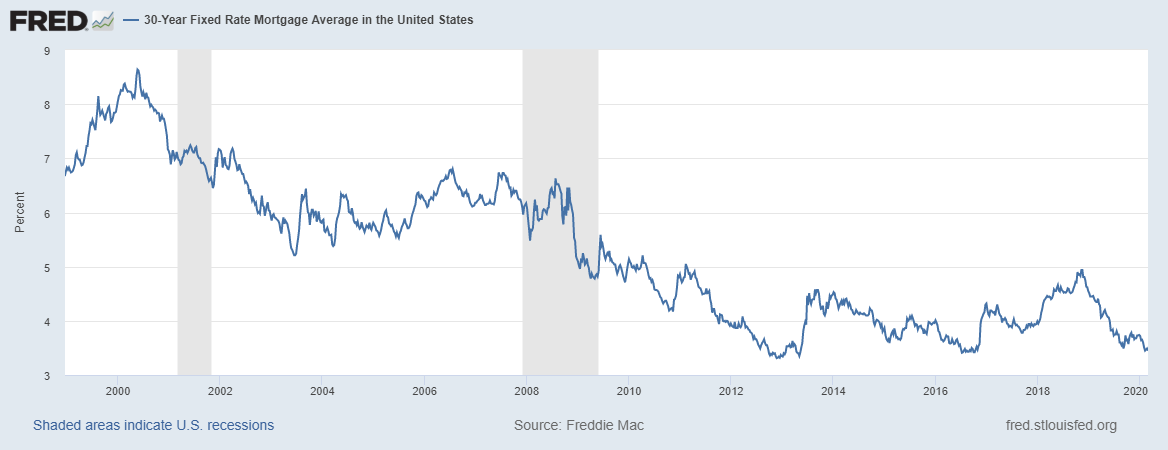

With 30-year fixed mortgage rates currently averaging below 3%, it might make sense for homeowners to consider refinancing. Depending on several factors, such as your current interest rate and age of your existing mortgage, refinancing could mean a lower monthly payment and big savings over the life of the loan.

Source: Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, March 1, 2020.

Should you refinance your mortgage?

Interest rates are very low right now, so unless you bought or refinanced in 2012 or 2013, odds are your rate is higher than what you could get today, assuming no changes to your credit or income that might negatively impact your profile as a borrower. When you refinance a mortgage, you get a new loan and use the proceeds to pay off your existing mortgage. The principal is typically your current outstanding mortgage balance and the loan will be re-amortized over a new period, perhaps 30 years.

Refinancing your mortgage can be a great way to increase your monthly cash flow and pay less in interest over the lifetime of the loan. But before rushing off to speak with a lender, it’s helpful to understand how the potential benefits and drawbacks of refinancing can change relative to your personal situation.

When did you get your current mortgage?

When you first start payments on a fixed-rate mortgage, most of your monthly payment is interest expense, with a much smaller amount going to pay down your principal. As the years pass, more and more of your fixed monthly payment will drift towards paying down the loan principal.

Since so much of your monthly payment is interest expense at the beginning, refinancing a mortgage obtained more recently can provide greater savings to homeowners over the life of the loan (all else equal) compared to individuals who have had their loan for longer, as they’ve already gone through the years with the greatest interest expense and did so at the higher rate.

Although homeowners with a newer mortgage may see greater overall savings, individuals with an older mortgage will generally see the most significant drop in their monthly payment. As explained above, when you refinance, you’re getting a new loan. When homeowners refinance a longstanding mortgage, the new loan amount will be reflective of the principal they’ve paid to date. Combined with a lower interest rate, the savings can be substantial.

By way of example, consider two homeowners who both purchased a home with a $500,000 loan and 4.25% interest rate. Both are now considering refinancing at 3.25%. The first owner purchased in 2010 and the second buyer obtained a loan in 2018. All else equal, the first homeowner will have a smaller monthly payment after refinancing.

How long will it take to break even on your closing costs?

As you might imagine, your potential benefit from refinancing depends, in part, on how much your new interest rate will change relative to your current one. The bigger the spread the bigger the potential savings. If you’re considering refinancing, a starting point for your cost-benefit analysis should be the payback period for your closing costs.

Lenders estimate that closing costs are generally between .75% and 1% of the loan. Although you can arrange for a zero-cost refinancing by paying a higher interest rate or rolling it into the principal, it will cost you more over the life of the loan. Further, the additional debt isn’t tax-deductible as it exceeds the existing loan balance. To calculate how long it will take to recoup your closing costs, divide the expected closing costs by the monthly savings from refinancing.

Using the example above and assuming closing costs are 1% of the loan, the payback period for homeowner one is a little more than five months, meaning they would breakeven on the cost of refinancing very quickly. In other situations, it can take years to break even on the closing costs, so you’ll need to consider how long you plan to own the home before deciding to refinance.

Also note that if your home is in a living trust, you will likely need to take the home out of trust to refinance.

Other considerations

Analyzing the cumulative benefits of refinancing a mortgage is a fairly complex exercise. In addition to the considerations raised above, the following factors also come into play:

- What will you do with extra cash each month? One component of the benefit analysis is what you decide to do with the extra cash in your pocket each month. Paying down other high-cost debt or investing for financial goals can increase the benefits of refinancing, but if the money is just spent on lifestyle expenses, your upside will be limited.

- Will refinancing impact your taxes? In 2021, the standard deduction is $25,100 for married couples and half that for single filers. Given that state and local taxes are limited to $10,000 per return, mortgage interest is usually the extra push that allows taxpayers to itemize their taxes so they can benefit from charitable deductions and other deductions only available to itemizers. Consult your CPA to discuss how refinancing could impact your tax situation.

- Tax law changes: Under the 2017 tax reform, when homeowners refinance the allowable interest will only be deductible for the remaining term of the debt that was refinanced. Previously, the interest would have been deductible for the full term of the new mortgage. Also, refinanced loans greater than $750,000 (but less than $1M) that were issued before 12/15/17 can keep their ‘grandfathered’ status for the mortgage interest deduction, provided the refinance does not increase the principal. While refinancing to a new loan with the same term as an existing mortgage won’t necessarily extend a mortgage interest deduction in perpetuity, it can offer investors greater flexibility to maintain a low monthly payment with the option—but not the obligation—to pay down the mortgage more aggressively each month.

Now may be a great time to refinance your mortgage and enjoy the flexibility of lower monthly payments. Although refinancing may seem like a hassle, depending on your current situation, it could (literally) end up paying off for years to come.

This article was written by Darrow advisor Kristin McKenna, CFP® and originally appeared on Forbes.