According to a recent survey of U.S. households by Schroders, only 27% of respondents who were still working reported ‘very good’ and ‘fully on track’ when asked how they feel about their retirement planning. Even more alarming, only 18% of workers between age 60 – 67 say the same. But how can you tell if you’re on track to retire and what should you do if you’re not?

Am I on track for retirement?

This is the (multi)-million dollar question. No matter where you are in your journey towards retirement, there are steps you can take to assess your progress and adjust. Exactly how impactful any changes may be depends primarily on how many years you have until retirement and the magnitude of the adjustments.

Here are five tips to help investors assess whether they’re on track to meet their goals and ways to jumpstart your retirement strategy.

Realize there’s no magic number

Having a certain amount saved for retirement doesn’t translate at all to how prepared that individual is to live the lifestyle they want in retirement. How much you’ll need to save for retirement depends on mostly on your expenses, not your savings. To illustrate, consider the following simplified example, which excludes factors like inflation, market volatility, etc.:

A portfolio of $1,000,000 grows 5% annually and the retiree withdraws $120,000/year. The assets are depleted in the 12th year. However, if the retiree limits the withdrawal to $75,000, the money would last almost twice as long.

It’s the same million dollars, but the outcomes are quite different. It’s also a great example of a controllable factor: spending. If you’re underprepared for retirement and concerned about running out of money, reducing your expenses can go a long way.

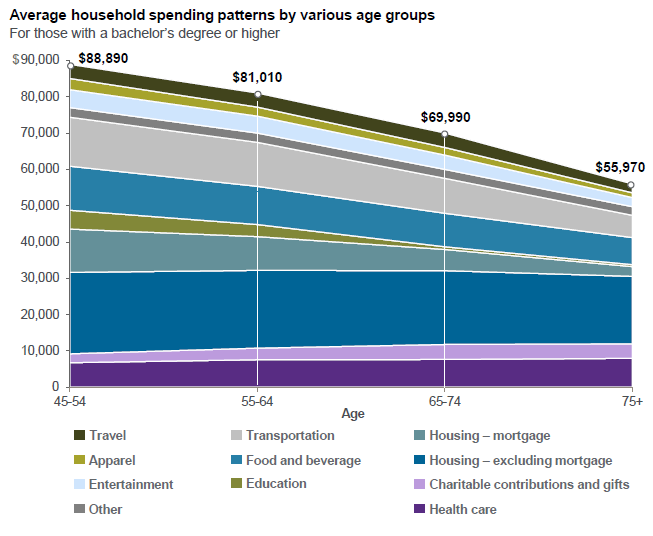

Don’t overestimate your retirement expenses

Retirement marks the end of a lifetime of saving for it. Pre-tax contributions are taken from your paycheck before you ever see it, so it’s easy to overlook the impact on your take-home pay.

These contributions are substantial: in 2021, a couple over 50 could save $52,000 in a 401(k) this year alone. When estimating your income needs in retirement, it’s important to account for big outflows that will disappear when you stop working.

It’s also a misconception that expenses only go up in retirement. Spending usually peaks around age 50 and declines over time. While expenses like housing and healthcare remain significant during life, virtually all other spending categories tend to slowly decline.

A big part of getting on track for retirement comes down to your investment strategy

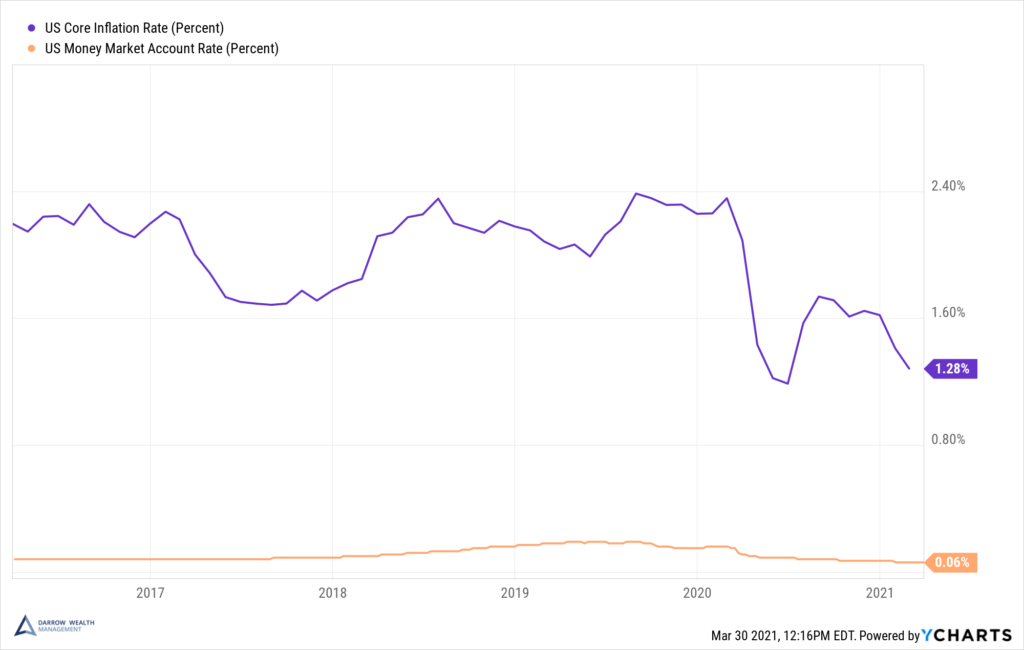

According to the survey, nearly half of pre-retirees said they had ‘no idea’ how they were invested. Respondents also report over 25% of their retirement assets are in cash. Cash!

Sitting in a money market account doesn’t build wealth – it erodes it. Here’s the US core inflation rate (goods and services, excluding food and energy) compared to the US money market account rate over the past five years:

Keeping a lot of cash might seem like a safe play, but you need to consider the loss of purchasing power. Typically, investors are overweight cash when they’re not sure what else to do with it. Having the right asset allocation is an essential part of getting on track for retirement. For most investors, that means exposure to stocks and bonds.

On the other side of the coin is taking too much investment risk. Trying to catch up by investing too aggressively or holding too much stock in one company can make the problem much worse.

Accept that working forever isn’t a retirement plan

A study from the Urban Institute found over half of full-time workers over 50 experienced involuntary job separation with their long-term employer, leading to prolonged unemployment or a reduction in earnings of 50% or more for at least two years. After rejoining the workforce, only 8% of college grads were able to get back to their pre-separation salary.

According to another study, from the Employee Benefit Research Institute, the median estimated retirement age is 65, but the actual median age is 62. Health issues and company downsizing/closing were the top reasons for retiring early.

Being realistic about the likelihood of not being able to work ‘forever’ or even until normal retirement age is part of a prudent, risk-adjusted retirement plan. Unfortunately, it’s not always about how long you want to work for, rather how long you actually can.

Make adjustments using different retirement levers

Regardless of the size of your retirement nest egg, it’s important to focus on what you can control when trying to plan for the decades to come. Particularly if you’re only starting to plan for retirement later in life, using multiple retirement levers can help get you on track.

Here are some factors to consider:

- Dynamic spending plan. Keeping fixed costs manageable can allow retirees to make adjustments to their income needs depending on how the portfolio performs. This can help reduce the impact a market downturn can have on your portfolio.

- Avoiding major purchases at the beginning of retirement. Sequence risk describes how the order of investment gains or losses and timing of cash flows affect portfolio values. Big withdrawals at the beginning of retirement can have a lasting impact on your plan.

- Develop a tax-efficient retirement income plan. Consider the pros and cons of using retirement accounts to delay Social Security, blending withdrawals from retirement and taxable brokerage accounts before RMDs, and using asset location strategies to add layers of tax-efficiency.

- Working longer while you can. While this isn’t 100% in your control, working longer or delaying an early retirement can make a huge impact on your retirement outlook.

- Boost your savings rate. If you have many more years until retirement, improving your savings rate is going to be one of the best ways to get on track for retirement. For high earners, just maxing out your 401(k) may not be enough.

There’s no one-size fits all solution for everyone. And it’s important to realize that any single approach is unlikely to be a cure-all. But in exploring alternate strategies, along with fundamentals like having a high savings rate and keeping expenses in check, you can help get your retirement plan on track.

Don’t let perfect be the enemy of the good

Not knowing where you stand financially or if you’re on track for retirement can be stressful. But rather than spend time wishing you started saving earlier, or keep kicking the can with the intention to do robust retirement projections later, take control of your current situation now. Dig into your finances. Look at your spending, asset allocation, and how much you’re saving and where. Run some projections to get a sense of where you stand. Even if you’re not working with a financial advisor, there are still steps you can, and should, take to improve your retirement plan.

This article was written by Darrow advisor Kristin McKenna, CFP® and originally appeared on Forbes.