What is a brokerage account and why should I open one? How is a brokerage account taxed?

Brokerage accounts (also called non-qualified accounts) are taxed differently than qualified retirement plans like a 401(k) or a 403(b). Even without taking money from the account, your brokerage account will be subject to tax each year. Here is a specific example of how a brokerage account is taxed and when taxpayers may span multiple long-term capital gains tax brackets. Plus, 9 reasons you need a brokerage account to fund a high-income lifestyle before and during retirement.

Taxes on income in a brokerage account

A brokerage account can be subject to tax in two ways:

- From trading activity (e.g. selling positions to rebalance or to withdraw money)

- Income from dividends, interest, and/or capital gains distributions

As an investor, you can control the tax timing for trading activity, though as discussed later, don’t let the tax-tail wag the dog here. However, when investing money through a taxable brokerage account, income from dividends, interest, and capital gains distributions from mutual funds will be subject to tax the year it is received. This is true regardless of whether the income was received in cash or automatically reinvested fractional shares or whether you take money out of the account.

Since a brokerage account is such an important component to building wealth that can sustain a high-income retirement lifestyle, try not to get too hung up on paying taxes along the way. For investors without a large cash flow surplus from their outside income, we advocate the account pays its own way as far as taxes go. Though it might be impossible to calculate the account’s precise tax liability, it isn’t hard to estimate it. When you have the figure, consider taking the funds out of the taxable account to reimburse yourself.

Taxes on sales in a brokerage account: short-term versus long-term capital gains

Capital gains tax is considered either short or long-term. In most cases, your holding period (how long you own the asset) will determine whether the gain or loss is classified as short or long-term for tax purposes. Holding period matters a lot as it’s a major factor in your capital gains tax rate. The tax code favors long-term ownership.

Calculating your holding period

In general, if you hold an asset for one year or less, your capital gain (or loss) is short-term. If your holding period is more than one year, your capital gain or loss is long-term. To calculate your holding period, you start counting beginning the day after you purchase or acquire an asset. The day you sell the asset will count towards your holding period.

Short-term vs long-term capital gains tax rates

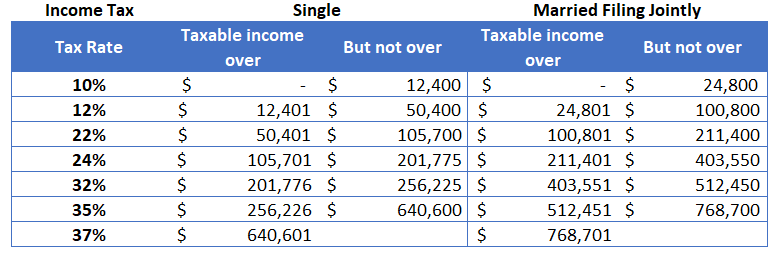

As previously mentioned, the long-term capital gains tax rate is much more favorable than the short-term rate. If you have a short-term capital gain, the tax rate is the same as your regular income tax rate.

2026 Tax Brackets for Regular Taxable Income, Short-Term Capital Gains, and Ordinary Dividends

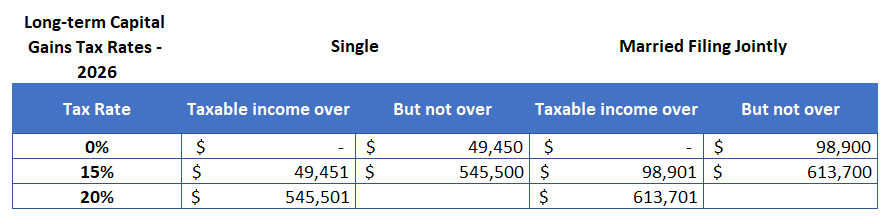

2026 Long-Term Capital Gains Tax Rates and Qualified Dividends

The tax rates are based on taxable income and don’t correspond exactly to regular income rates. To determine your long-term capital gain tax rate, you’ll stack your long-term capital gain on top of your regular taxable income. The combined total determines the tax bracket(s) the gain falls in.

How to determine your tax bracket for long-term capital gains

For illustrative purposes, it may be helpful to know how long-term gains integrate with your regular income. In practice, it’s more complicated than this. So you’ll want to work with a CPA or use tax preparation software to calculate your taxable gain and the impact on your entire tax situation.

The illustrative examples below are using the 2026 tax year and exclude any state or other taxes.

Example #1: one rate for long-term capital gains

Married couple filing jointly with taxable regular income of $200,000 and a long-term capital gain of $50,000. Assume the couple takes the standard deduction, $32,200 in 2026, and has no other credits/deductions.

For ordinary income, the couple is in the upper half of the 22% tax bracket with net taxable income of $167,800 ($200,000 – $32,200).

For long-term capital gains, this puts the couple in the 15% bracket with plenty of room before the next tax rate increase. To estimate the federal tax due on capital gains, multiply $50,000 * 15%.

Example #2: two rates for long-term capital gains

Assume the same facts as the previous example, only the couple’s regular taxable income is $100,000. After the standard deduction, the remaining taxable income is $67,800. This is $31,100 below the threshold for the 15% tax rate on long-term capital gains.

The couple now falls into two tax brackets for long-term capital gains. There is $31,100 remaining in the 0% bracket. The remaining $18,900 will be taxed at 15%.

Simplified examples and hypothetical calculations for illustrative purposes. Not tax advice.

Strategies to Reduce Capital Gains Taxes

How to net capital gains and losses

If you have capital losses and gains, you will need to find the net gain or loss before you can determine the impact to your tax situation. The process for netting capital gains first applies to gains and losses of the same holding period. For example, long-term gains and losses are netted against each other, and separately, short-term losses reduce short-term gains. If the resulting short-term and long-term figures involve a gain and a loss, they are netted again.

Example: netting capital gains and losses

Short-term calculation

Investment A = $40

Investment B = ($50)

Total short-term loss = ($10)

Long-term calculation

Investment C = $5

Investment D = $10

Total long-term gain = $15

The short-term loss ($10) is netted against the long-term gain of $15 to result in a net long-term gain of $5 and no short-term gain. If the long-term figure above been a loss instead of a gain, the taxpayer would have had both a short and a long-term loss.

Net losses can potentially reduce ordinary income by up to $3,000 in the current tax year. The remainder (if any) can be carried forward as a deduction in future years.

Note that this is a highly simplified example and on your tax return, gains and losses from most other asset types are included in the calculation, not just stocks and bonds.

Simplified examples and hypothetical calculations for illustrative purposes. Not tax advice.

What is a brokerage account?

A brokerage account is a non-retirement investment account. Essentially, a brokerage account is the opposite of a retirement account like an IRA or 401(k) in nearly every way. There are no restrictions (income, investment options, limited additions, access, etc.) or tax benefits.

Because there are no income restrictions or funding limits, a taxable account provides the most flexible option for investing extra money. Unlike retirement accounts, there are no rules about when you can take money from a brokerage account or requirements forcing you to do so.

Investing money in a brokerage account gives you the most flexibility compared to other types of investment accounts. The account is funded with after-tax dollars, like savings in your bank account. There’s no tax deduction for contributions. You can invest money as often or infrequently as you like. Open a brokerage account at one of the major financial institutions or with the help of a fee-only financial advisor.

A brokerage account is usually the best way for individuals to invest for medium-term non-retirement goals such as college, a home, major asset purchase, or just because they have extra cash flow or savings. For retirement goals, a brokerage account is often key in helping fund an early retirement or supplement retirement savings so affluent individuals can maintain their lifestyle.

Why put money in a brokerage account? 9 reasons

A brokerage account is a popular type of investment account due to the flexibility it affords. With no income restrictions or funding limits, a taxable account provides the most options for investors. Further, unlike retirement accounts, assets in a brokerage account can be used for any purpose at any time without early withdrawal penalties. While it usually makes sense to max out a retirement plan at work first, here are some of the benefits of investing money through a brokerage account.

9 reasons to open a brokerage account

No contribution or income limit. Free of usual retirement restrictions governing contribution limits or income-based rules on deductibility or access.

Liquidity and flexibility. Flexibility to use the money when you want without penalties is key for pre-retirement goals and access to money if you want to retire early. Invest for things like college, home renovation, or anything else you might need before retirement. A brokerage account can also be a great way to invest extra savings or a lump sum after a windfall or liquidity event.

Favorable tax rates. Ability to benefit from more favorable long-term capital gains tax rates. For high earners, this will be lower than ordinary income rates, especially gains that fall into the 0% tax rate.

No RMDs. No required minimum distributions in retirement. Traditional IRAs, 401(k), 403(b), pension plans, etc. all force retirees to begin taking the money out in their 70s. Or even earlier on many inherited accounts.

Legacy planning. Tax-efficient way to leave a legacy due to the step-up in cost basis. This increases or ‘steps up’ their inherited cost basis in the asset to the value on the date of your death. This is a major tax benefit for investors with large taxable accounts with unrealized gains as their heirs may never need to pay tax on the growth (up until the account owner’s death).

Tax-loss harvesting. Ability to reduce tax on realized gains or accrue tax assets before a windfall by harvesting losses. Turn market volatility into a tax benefit by realizing losses to offset gains or up to $3,000 of ordinary income.

Direct indexing. Supercharge tax-loss harvesting with direct indexing, sector tilts, company exclusions, etc. Direct indexing is an investment strategy where the underlying stocks that comprise an index, like the S&P 500, are purchased instead of an ETF or mutual fund tracking the index. Using it for tax-loss harvesting can optimize after-tax returns because losses on individual stocks can be isolated and harvested, even when the entire index has gains.

Borrowing. Leverage your portfolio for cash without selling with an asset-based loan. “Tax-free” liquidity through Securities-Based Lines of Credit (SBLOCs). You can borrow against your portfolio for a major purchase without selling assets and triggering a capital gain or selling out of the market.

Build wealth! Retirement accounts alone won’t be enough to replace a high-income lifestyle in retirement. High-earners are limited to the same 401(k) contribution limits as individuals who earn significantly less. Because expenses tend to increase with income, wealthier individuals generally require more savings to continue their living expenses in retirement.

Main drawbacks of taxable accounts

- No tax deduction for contributions

- Account does not grow tax-deferred

Your overall wealth strategy

As you weigh the merits of a brokerage account, also consider whether it’s worth it to work with an investment advisor to help ensure you are making the most of your financial opportunities. As with any financial decision, you’ll want to make sure it aligns with your overall wealth strategy.

[Last reviewed January 2026]