Investing your 401(k) in company stock can be quite risky. Although companies are scaling back on the practice, there are still many big U.S. firms that allow participants to buy employer stock in their retirement plan or that make matching contributions in the form of company stock. Employees unaware of the potential consequences of their concentrated equity position are exposed to a great deal of risk. As evidenced over the years by the aftermath of the Enron scandal, RadioShack bankruptcy, and Wells Fargo scandal, employee participants could have their retirement savings decimated.

Is it common to have a 401(k) invested in company stock?

Thankfully, it is becoming less common for employers to invest employees’ retirement assets in company stock. However, many large U.S. companies are still doing it. According to Bloomberg’s ranking of retirement plans, in 2014, one in five of the largest companies in the S&P 500 made 401(k) contributions in company stock. Bloomberg also reports that nearly 70 percent of plans don’t have limits on how much participants can invest, based on data from the Plan Sponsor Council of America. According to Aon Hewitt, 60 percent of employers with stock on a public exchange provide company stock as an investment option for employees in the plan.

The dangers of having company stock in your 401(k)

Buying single stocks is a risky proposition in itself. Single stocks are exposed to a number of risk factors that could otherwise be diversified away – external factors such as industry, legislative, and regulatory can have a great impact on a company’s ability to compete in the market. Further, there are risks that the company itself may cause its own demise.

Recall the Volkswagen emissions scandal and Lumber Liquidators laminate flooring cancer scare. If you have upwards of 10% of your investments concentrated in one company, your financial future can literally be tied to theirs.

The inherent risks in owning individual equities are magnified when that company is also your employer. You already rely on the company to pay your salary and cover other job-related benefits like health insurance, so why would you also want to bet even more on the company and put your ability to retire at stake?

History has plenty of painful lessons for employees – a company can experience terrific growth for decades and one event can cause it to lose 40%, 60%, or more of its value overnight. Without liquidating your shares and diversifying into other investments over time you not only missed out on all the growth years, but you could be left with almost nothing.

It’s not all bad news though. Net unrealized appreciation can offer tax benefits if you have company stock in your 401(k)

How much company stock are you really holding?

Having company stock in your retirement plan may just be one way you own employer equity. Employees may have stock options like ISOs or NSOs, restricted stock units (RSUs), or buy shares through an employee stock purchase plan (ESPP). If you participate in multiple forms of equity ownership with your company, you may not realize how undiversified you are. In general, you should not have more than 10% of your net worth invested in any singular stock across all types of ownership vehicles – especially including your employer’s.

Ways to diversify out of a concentrated stock position

How you own the stock will dictate your options to divest:

- Elective contributions in your retirement plan: there’s typically a lot of flexibility to divest from funds you selected. Depending on the plan documents, you may be able to buy and sell securities at any point or update your allocation quarterly.

- Non-elective or matching contributions from your employer: if your employer makes matching contributions to your retirement account in company stock instead of cash, you may not be able to diversify right away. Depending on how the plan is set up, you may have to wait until you have three years of service at the firm to divest. This isn’t universally the case though; some companies may allow you to diversify immediately.

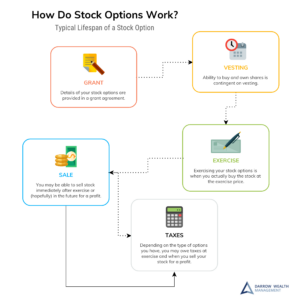

- Stock options: as the name implies, with stock options, you decide whether to exercise or not. If the options are underwater once they vest (the grant price is higher than the current market value) the choice is very easy: don’t exercise yet. If the market price is higher than the grant price and you choose to exercise, there are still ways you can mitigate your risk. If the spread between the market price and the grant price is great enough, you may be able to sell your shares immediately after exercising your options and profit in a quick, low-risk transaction. Speak with your financial advisor and tax professional before exercising your options as there may be tax consequences.

- Restricted stock units (RSUs): Because they are awarded to employees, RSUs have greater flexibility and potential upside than traditional stock options. But be careful in how you view them – just because you didn’t have to buy the stock out of pocket doesn’t mean you should take on added risk. Employers include equity options or awards as part of a compensation package for a number of reasons – one of which is to reduce their fixed salary obligations. Although you can’t diversify unvested awards, upon vesting you’re free to divest of the company stock (assuming your company isn’t going through an IPO or merger or acquisition). Consider liquidating at least a portion of your stock once vested to diversify into other investments. Remember, there are two ways to “leave money on the table” with restricted stock units.

- Own stock in an employee stock purchase plan (ESPP): if you participate in an ESPP you have the ability to reduce your concentration in company stock in two ways. First, change your payroll deductions to reduce or eliminate future participation in the plan. The plan documents will indicate how often this can be done, but typically it is very quickly. Second, you can sell all – or a portion of – the shares you already own through the plan. The tax consequences of selling shares will depend on whether the plan is a qualified Section 423 plan or nonqualified. Work with your financial advisor and tax professional to evaluate the potential tax consequences and develop a plan to liquidate the shares.

As with so many things, owning company stock is generally best done in moderation. Although you may not be able to fully control your exposure, there are still plenty of ways to mitigate your risk. To discuss a diversification strategy for your situation, please contact us to set up a free consultation.