Declines in the financial markets are an uncomfortable part of investing. Taking steps to plan ahead of a market decline is best, though what you do during a selloff is also crucial. Especially for equity investors, avoiding losses entirely is unrealistic. But individuals sometimes make decisions that cause preventable financial losses. Here are three ways to reduce the risk of incurring unnecessary, self-inflicted losses in a down market.

Single stocks ≠ the stock market

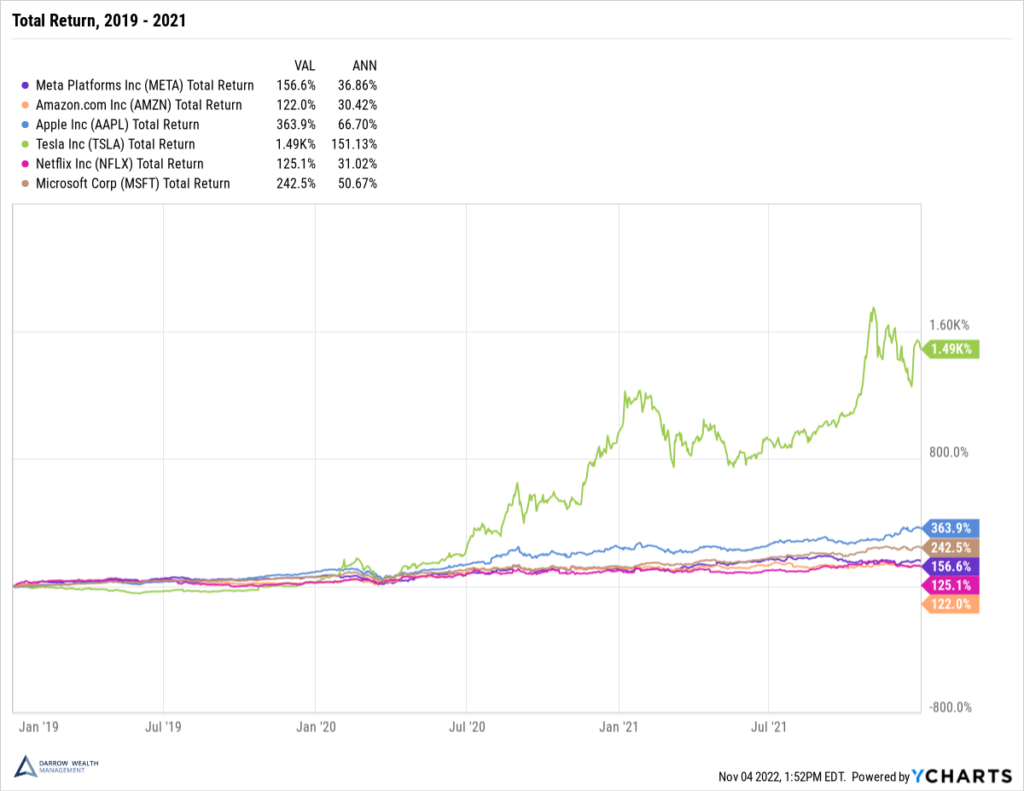

You’ve heard it before: past performance is not indicative of future results. It isn’t just legalese – it’s true – and the chart below shows why. this point. After years of strong performance…

…newly public companies and seasoned stocks alike have experienced stunning drawdowns. Compare these drawdowns to the Russell 3000 and suddenly the stock market doesn’t look that bad.¹

For single stocks, drawdowns like this aren’t uncommon. According to JP Morgan, between 1980 – 2020, roughly 45% of stocks that were ever in the Russell 3000 fell 70% or more from a prior peak and never recovered. Almost a coin toss.

Make no mistake, investing in one company (perhaps from employer stock options) can potentially yield massive gains, well beyond a diversified index. The issue is when investors don’t right size their risk, understand their exposure, or know when to take profits.

Checking your accounts can do more harm than good

One way investors incur unnecessary losses is by checking their portfolio during market downturns. To illustrate, the chart below plots the one-year total return for the S&P 500. The purple line shows daily gains and losses while the orange line reports monthly.

Both have the same net result.

But if you were checking your account every day you’d have a lot more ups and downs to deal with. Wild swings in the market will stress you out at best, and at worst, prompt you to make hasty investment choices that may create self-imposed losses.

So if you aren’t planning to make a change, what’s the point of looking? If there’s a reason to trade, make sure recency bias isn’t influencing the decision.

Chasing the market

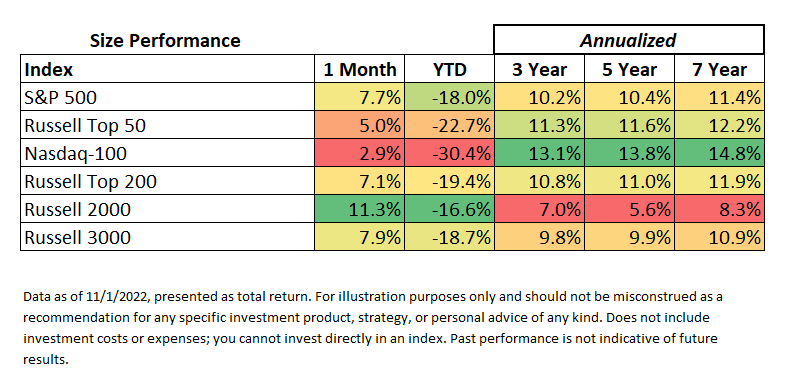

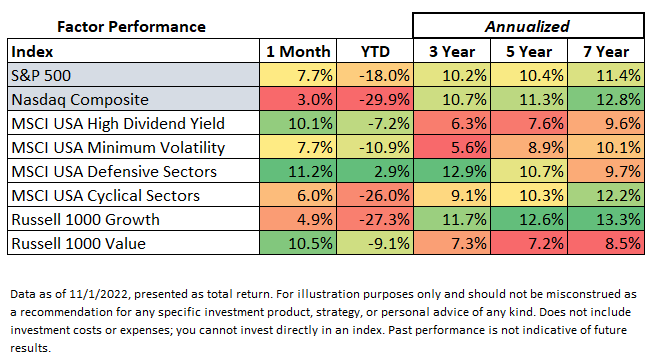

It can be tempting it can be to make changes to your portfolio after recent events. Looking at various equity indices for company size and factors, there’s little correlation between the best or worst performers in the past month or year versus longer periods of time. In fact, recently, the outcome is reversed.

The one-month return of small cap, high dividend, and defensive sectors, and value are particularly stunning. Yet going out seven years, these indices are the worst performers. Does that mean you shouldn’t have investments with these characteristics in your portfolio? No! It simply shows the importance of diversification. Markets are cyclical.

If you’re looking at your account daily, it’s tempting to sell the losers and chase the winners around. This can have lasting implications. These charts also highlight the downside of tax loss harvesting. Harvesting losses only for tax purposes can have broader implications due to the wash sale rules.

If you sell an investment for a loss, you can’t buy the position (or one substantially similar) back for 30 days. So you’ll either buy something you don’t like as much or stay in cash. The market may move significantly during this time – four indices above have gains over 10% in a month.

This isn’t an anomaly, either. According to Bespoke Investment Group, since 1928, the S&P 500 averages a 15.2% return in the first month of a bull market. Over the first 3 months, the average gain increases to 31.6%. What the market will do coming out of the 2022 bear market is anyone’s guess, but historically, markets move quickly, and the best days in the market often fall within a week or two of the worst ones.

Silver lining! Market shifts can bring opportunities

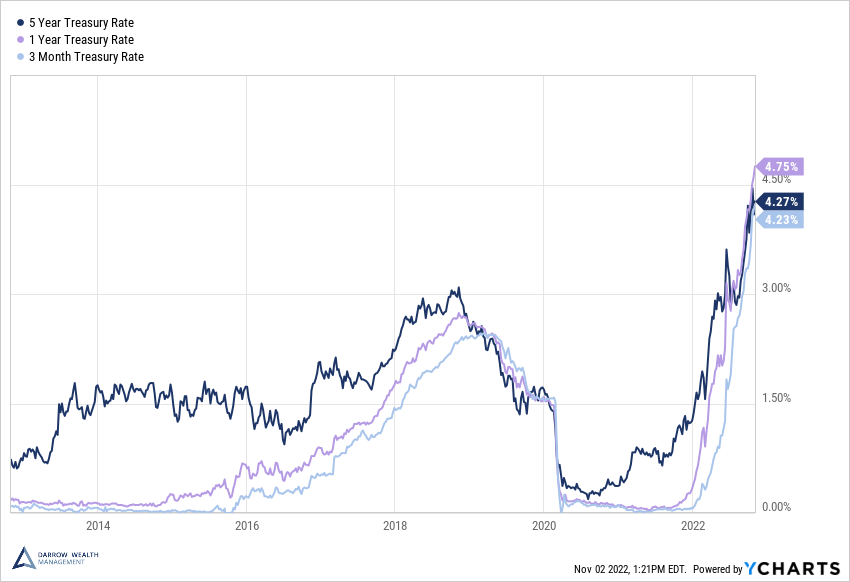

Changing market conditions may not be all bad news. Rising interest rates have been very bad news for stocks, bonds, and homebuyers. But, for individuals with cash, it’s a big win. One-year Treasuries are now yielding 4.75%…versus .17% a year ago (November 2021). That’s a 2,700% increase! Investors can create a Treasury ladder or just buy longer maturities to lock in the return.

Even high-yield savings accounts are giving a decent return on cash. There’s no reason to park lots of cash in a 0% checking account earning no interest when you can enjoy a safe 3% APY in the right savings account.

However, not suggesting individuals dump their portfolio and buy Treasuries! But for some investors, yields are attractive enough where Treasuries should be part of the conversation when considering allocation for a new cash investment.

It also highlights the nuances in investing and why few things are black and white. Don’t check your account daily doesn’t mean don’t ever check. And a passive buy and hold strategy shouldn’t ignore rebalancing needs, the right tax-loss harvesting opportunity, or periodic fund evaluations.

In down markets, there’s a tendency for people to want to to act. To do something to stop the losses. Acting on this urge often (though not always!) turns out to be an unwise decision. It’s also perhaps the most common way investors managing their own portfolio incur preventable financial losses.

Article written by Darrow Advisor Kristin McKenna, CFP® and originally appeared on Forbes.

¹ Total return percent off high, Russell 3000 drawdown roughly -22% to 11/3/2022. The Russell 3000 represents roughly 97% of the US equity market.