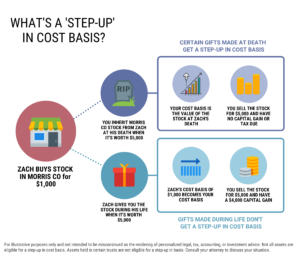

Losing a spouse is a difficult time, and navigating the complexities of inherited assets can feel overwhelming. If your spouse named you as the sole beneficiary of their traditional IRA, understanding your options is a crucial first step.

Here are the two most common distribution options after inheriting an IRA from your spouse as the sole beneficiary:

-

- Treat the individual retirement account as your own and roll the money into an IRA account in your name

- Transfer the assets into an inherited IRA

Important factors in determining the best approach:

- How old the deceased account holder was when they died

- The age of the surviving spouse

- Age gap between the account owner and spouse

- Financial situation of the survivor and their cash needs

- Whether the inherited IRA was a traditional IRA or a Roth IRA

Detailed Options for a Spouse Inheriting an IRA

The two most common spousal inherited IRA options are discussed below.

Important notes on the IRA rules:

- The options below reflect situations where the spouse inheriting the IRA is the sole primary beneficiary. Differences exist when multiple beneficiaries are listed as primary or current beneficiaries.

- Life expectancy methods below refer to IRS tables (Uniform Life Table or the Single Life Table) which are used in RMD calculations. The Single Life Table typically results in higher mandatory distributions.

Move the Money into Your Own Traditional IRA

- Distribution Rules: As a spousal beneficiary, if you roll inherited IRA assets into an account in your name, required minimum distributions (RMDs) will be based on your own age and life expectancy, regardless of the deceased account holder’s age. Note that if the deceased account holder had not yet taken their RMD for the year of death, that distribution must still be taken.

- Advantages: This is often the most straightforward option. It can be particularly advantageous if:

- Spouses were of similar age or the survivor is younger. This is due to how RMDs are calculated and prolonging tax deferred growth.

- You eventually remarry or have eligible designated beneficiaries*, it provides greater flexibility for future beneficiaries to take distributions.

- Important Consideration: Distributions taken before age 59 1/2 are subject to the early withdrawal penalty.

Transfer to an Inherited IRA

- Distribution Rules: The distribution rules for inherited IRAs are more complex and depend on a few factors, most notably whether the original account holder died before or after their required beginning date (also known as RMD age, currently 73 for those born from 1951 to 1959).

- Death Before RMD Age: RMDs are typically delayed until the original account owner would have reached RMD age. After that, distributions are calculated using the surviving spouse’s life expectancy.

- Death After RMD Age: RMDs must begin the year following the death of the original account holder. The amount is based on the longer of the survivor’s life expectancy or the deceased account owner’s life expectancy. Again, any undistributed RMD from the year of death must be taken.

- Advantages: Using an inherited IRA can be beneficial in specific situations:

- When the surviving spouse is under age 59 1/2 and needs access to the funds without incurring early withdrawal penalties.

- When the surviving beneficiary is much older than the deceased IRA owner. This is because the RMD rules may allow the surviving spouse to further delay recognizing ordinary income and/or calculate required minimum distributions using the original IRA owner’s longer life expectancy.

- Important Consideration: Due to the complexity of the rules and nuances, it is crucial to discuss your specific situation with a financial advisor, estate planning attorney, and tax professional. It’s also worth noting that an inherited IRA can be rolled into your own IRA before required distributions begin, offering another tax planning opportunity.

Other Inherited IRA Account Options After a Spouse’s Death

Move assets to an inherited IRA and later roll the funds into your IRA

- When to consider: To avoid early withdrawal penalties initially, potentially benefit from distribution rules for non-spouse beneficiaries if you remarry, and delay RMDs based on the deceased spouse’s age before eventually rolling the funds into your own IRA for your future beneficiaries.

Roll the assets into an IRA in your name and consider Roth IRA conversions later

- When to consider: Roth conversions are often considered as an income tax planning strategy as controlled conversions can help avoid pushing you into a higher tax bracket when you must start taking distributions. Roth conversions reduce asset balances subject to mandatory withdrawals and if holding periods are met, money can be taken out tax free. Required minimum distributions cannot be converted to a Roth IRA.

Take the money as a lump sum distribution

- When to consider: If you need liquidity now or if the inherited IRA assets are not significant and there’s no 10% early withdrawal penalty.

Disclaim the inheritance (in full or in part), allowing the money to pass to other beneficiaries

- When to consider: If you don’t need the inherited account to support your own financial goals and/or if you’re working to reduce your own estate for state or federal estate tax purposes.

Paying Taxes on Annual Distributions

Planning is so important after the account owner’s death because withdrawals from tax-deferred retirement accounts are taxable as regular income. If you need the cash flow and there aren’t any other inherited assets, then this type of income tax planning may be moot. Though, you’ll still want to discuss with your financial and tax advisor.

However, if you did receive other inherited assets or if you already have enough wealth in your name, it can be beneficial to delay taking RMDs after the account holder’s death, plan pre-RMD withdrawals to avoid getting pushed into a higher tax bracket later, or simply give yourself as much flexibility as possible by reducing annual distributions as much as possible.

Checklist: What to do After the Death of a Spouse

Considerations for your IRA Beneficiaries

A complete discussion of the inherited IRA beneficiary rules is outside the scope of this article. However, it’s something to discuss with your attorney and financial advisor. After the Secure Act, most non-spouse beneficiaries who inherit a retirement account can no longer ‘stretch’ the distributions over their lifetime.

Instead, most non-spouse beneficiaries must follow the 10-year rule, when inherited IRA assets must be fully depleted. Whether they must also take distributions during this window will depend on whether the original account owner died before their required beginning date and whether the money was moved to the spouse’s own IRA or an inherited IRA. The specific facts and circumstances could also further shrink the 10-year window and negate typical options for surviving spouse beneficiaries, if you remarry.

Getting Financial Help

At this stage, it’s typically best to stay focused on your own financial needs and goals. However, since the decision to move the money to your own account is irreversible, it should be considered. Don’t rush into important financial decisions and consult with financial and legal professionals who can help secure your financial future. For help navigating your path forward, please contact us to schedule a consultation.

*Other than surviving spouses, are three exceptions to the 10-year rule for eligible designated beneficiaries:

- Minor children have until they reach the age of majority (21) before the 10-year payout period begins

- Beneficiaries less than 10 years younger than the decedent, or

- If the beneficiary is disabled (strict definition applies)

Beneficiaries qualifying for exception #2 or #3 can take the funds over their lifetime called a stretch IRA.

[Last reviewed May 2025]