Estate planning is the process of preparing wills and other legal documents to distribute your assets and make arrangements for your wishes to be carried out in the event of your death or incapacitation. Given the subject matter, it is not surprising that many individuals aren’t exactly eager to participate. If you’ve ever heard a second or third-hand horror story about someone dying without a will or with a stale beneficiary designation, you might have been tempted to think: Wow, that’s terrible…but I know that would never happen to me.

The truth is: without a proper estate plan, these moments of financial reckoning can – and likely will – happen to your loved ones. We cannot control when our time is up – but we can control what type of legacy (or mess) we leave behind.

From the experts: true stories of estate planning nightmares

From the experts: true stories of estate planning nightmares

From the experts: true stories of estate planning nightmares

From the experts: true stories of estate planning nightmaresOne of the reasons individuals delay getting an estate plan in place is that they just don’t realize the consequences to their loved ones of not having one. After all, you don’t know what you don’t know. To help illustrate some of these commonly-unknown situations and misconceptions about trusts that could have been avoided through estate planning, we have asked a couple of estate planning attorneys in Massachusetts to share some of their stories.

Probate means more of your liquid assets will go to the state; less available for your loved ones

When individuals die without a will, or they own assets in their own name at the time of their death that will not pass to heirs via beneficiary designation, these assets will go through lengthy, expensive, and public probate court proceedings. Through proper planning during life, these situations could almost always have been avoided.

“Probate administration at death cares little about the value of your assets. Of course some of the filing fees are based on value, and very valuable estates with complex assets can be more expensive to administer, but in general whether an estate is worth $100,000 or $1,000,000 is likely going to cost the same amount. Not having an estate plan may be the cheapest option while you are alive, but it is going to be the most expensive to administer at your death – taking away more from your beneficiaries. The client who creates a simple will will also saddle their beneficiary with unnecessary administration costs, but slightly less than someone without a plan. The client who creates a trust and pays a little more out of pocket during life, will save their beneficiaries thousands (to tens of thousands) in administration costs.”

– Kristin N.G. Dzialo, Esq., Partner at Rubin and Rudman, LLP in Boston, MA

Doesn’t the surviving spouse automatically inherit everything – even without a will?

Not so fast. When you die without a will, each state will have its own laws about how the assets in the decedent’s probate estate will pass to surviving heirs and beneficiaries:

“Most people assume that a surviving spouse will inherit everything from their deceased spouse (even if the decedent passed without a will, known as dying intestate). While this may be true in certain circumstances, each state has what is known as an intestacy statute that dictates who inherits from a decedent dying without a will, and the answer might very well surprise you.”

– Brett J. Barthelmeh, Esq., Partner at Squillace & Associates in Boston, MA

Even for married couples without children, not having a proper estate plan in place can cause unnecessary emotional and financial stress for the surviving spouse. Especially in situations where an adult child predeceases their parents, the living spouse may not receive the inheritance intended.

“We work hard to make client meetings palatable; estate planning is hardly a favorite topic of conversation for most people. One of the things we often say to keep it light when scenario planning with clients is Ôthat could work, if everyone cooperates and dies in order’ – meaning grandparents passing before adult children, and adult children passing before grandchildren. But, since professionally we live in a world focused on the outer edges of the bell curve, we know this isn’t always the case. Our firm recently assisted a surviving spouse who was shocked to learn that because her wife died intestate, and the couple had no descendants, that the decedent’s elderly parents (living internationally) were entitled to a portion of their daughter’s estate. With proper planning you don’t need to rely on people cooperating and dying in order.”

– Brett J. Barthelmeh, Esq., Partner at Squillace & Associates in Boston, MA

Many estate planning issues can arise during your life

It’s a common misconception that an ‘estate plan’ simply refers to wills and perhaps a trust. When done properly with a qualified attorney who specializes in this area of the law, an estate plan will also include a power of attorney and health care proxy or power of attorney. These documents can help ensure your medical and/or financial needs and wishes are met in the event you are incapacitated and can no longer manage your affairs or participate in your care.

“I had a case where the father fell in his driveway and suffered from a traumatic brain injury. He did not have any estate planning documents in place, not even a health care proxy or power of attorney. After his hospitalization, he was at a rehab facility. The mother was quite frail herself and was suffering from a variety of health ailments. They had two children and the family was exceptionally close – the children were included on a few bank accounts as joint owners to help the parents. The father was unable to make medical or financial decisions for himself, so a guardianship and conservatorship proceeding was required. If the father had had those documents in place, then no court proceedings would have been necessary. The court decided to appoint an attorney to represent the father and that attorney was highly suspicious of the family and did not understand the financial planning the family was trying to undertake to ensure the father could qualify for MassHealth. The family ended up with a protracted legal battle with the father’s attorney – spending over $50,000 in legal bills. The father later regained enough consciousness to execute a health care proxy and power of attorney so the family was able to “get out” of the litigation. However, the father passed away a few months later. In the last months of his life, the family was spending time and money on legal matters instead of spending that time with their father.”

– Marlee S. Cowan, Partner at Rubin and Rudman, LLP in Boston, MA

Estate plan, meet desk drawer

It is an all-too-common scenario for individuals to spend the time and money on an estate plan and trust documents, only to immediately pop it into a desk drawer without actually funding their trust (retitling assets and updating beneficiary designations in the name of the trust). Without this critical second step, the whole plan often crumbles:

“Improper funding will require assets to pass through the probate court before passing to the trust. If the sole goal of the trust is probate avoidance, this can make the use of the trust and the cost to create it, completely pointless. Any assets that are individually owned, without a designated beneficiary, will have to pass through probate court. The will may then direct those assets to the trust, but one of the benefits of the trust is to avoid that probate process entirely. Ensuring that assets are directed to the trust through beneficiary designations and ownership is key to probate avoidance. It is imperative that that clients have an understanding of not only what documents are in place, but how their assets are connected to those documents.”

– Kristin N.G. Dzialo, Esq., Partner at Rubin and Rudman, LLP in Boston, MA

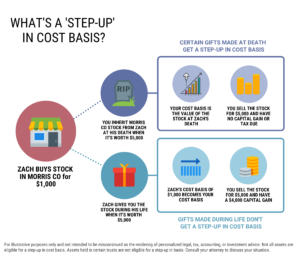

Even with funded trusts, an estate plan should generally be reviewed every few years. Your assets and goals can change – and the laws change too. Sometimes these changes mean complex planning is required, but as Kristin Dzialo explains, the dramatic increase to the federal estate tax exemption in 2018 has made some complex trust strategies no longer necessary or actually inconsistent with current objectives.

Sibling rivalry…or warfare

Without having the right plan in place before it is needed, situations can quickly go awry even when the family is all on the same side. But if the adult children don’t see eye-to-eye, and there isn’t an estate plan in place, the devastating reality is that the legal battle to follow will likely dent – or even drain – whatever funds were at stake to begin with.

As Marlee Cowan explains, sometimes the sibling power-struggle begins long before the parent passes away, forcing them to wait for needed care while the battle plays out in court:

“A mother suffered from dementia and had never put an estate plan in place. As she declined, a guardian and conservator was necessary to handle her medical and legal affairs. She had four daughters, three got along quite well; however, the fourth daughter was the ‘spoiled’ one. The daughters had a protracted legal battle regarding who should be the guardian and conservator for their mother, finally agreeing to appoint a family friend. A few months later, the mother was running out of money and the conservator needed to sell the mother’s home to raise sufficient resources for her care. The estranged daughter caused an enormous disruption to the process, again resulting in incredibly high legal bills and all at the expense of her mother. If the mother had implemented a health care proxy or power of attorney, her wishes would have been clear about which daughter she would have trusted to handle her affairs. Once the mother began to suffer from dementia, she could no longer express her wishes and it was up to the court to try and determine what the mother would have wanted. No one should want a court to make such an incredibly personal decision for themselves and, as difficult as it may have been for the mother to select one of her four daughters, it would have been less difficult than the inevitable vicious fight among the daughters – again, all at the mother’s expense.”

– Marlee S. Cowan, Partner at Rubin and Rudman, LLP in Boston, MA

What would a teenager do with a lump sum from a life insurance policy?

You might imagine several different ways…and it’s highly likely that investing the proceeds in a diversified asset allocation targeting long-term growth isn’t one of them. Even if the proceeds were largely squandered by a young teen – it’s difficult to fault them for it – they shouldn’t have been in a position to make such an important decision in the first place.

This situation becomes even more complex when a special needs child is also part of the equation:

“A client contacted me and told me that her husband had just died. They had two children, one age 14, and the other, age 12, was severely disabled. The husband had left a life insurance policy payable to both kids, and the life insurance company would not disburse funds to their mother as she did not have the proper authority to receive them on behalf of the children. We had to immediately file for a conservatorship for each child, so that the mother could access the funds, explaining to the court exactly what she intended to do with the funds. We prepared a (first party) special needs trust for the daughter and funded it with the insurance proceeds. With the other daughter, we had to file annual accountings with the court until she turned 18 and was no longer a minor, when the remainder of the money was then given to her.”

– Marco A. Schiavo, Esq., Partner at Simmons & Schiavo, LLP in Woburn, MA

No better time than the present, because it probably can’t be fixed later

In the previous example, Marco was able to help his client improve the outcome of a highly undesirable situation, but that’s not to say the result was optimal for the family (considering an 18-year-old teen was later given full access to the life insurance proceeds).

Since Marco didn’t have the opportunity to work with his client and her husband to get a better plan in place before he suddenly died, the ideal solutions for the family were no longer available:

“This could have been avoided by a properly drafted revocable trust. The life insurance could have been payable to the trust. A supplemental needs (third party) trust could have been included as part of the estate plan, which would not require a pay back to the government upon the child’s death. The distribution to the older child could have been made when she was older and more able to manage her money, perhaps in her late 20s or early 30s.”

– Marco A. Schiavo, Esq., Partner at Simmons & Schiavo, LLP in Woburn, MA

It’s the same principle as making sure your children wear a helmet when they ride a bike. If they fall and break their arm it will heal, but if they suffer a brain injury it could be irreversible. And perhaps they won’t fall at all – the point is that you just don’t know, but it isn’t worth the risk.

The right plan requires the right team of advisors

Developing and maintaining an estate plan that will meet evolving your needs and legacy goals requires the support of the right team of legal, financial, and tax professionals. As with nearly any profession, it’s important to work with an attorney who specializes in estate planning. You wouldn’t let your primary care doctor give you open heart surgery, would you?

Unfortunately, other times plans fail because an advisor or attorney took a shortcut or put their own interests ahead of their client’s:

“I had a will contest case that highlights the consequences of poor planning. The father had five children, and one was his primary caretaker. As such, the father left 80% of his assets to that child in his will. All other children received 5% each. The other children acknowledged that the primary caretaker was entitled to the majority of their father’s estate. However, they argued that there was no way that their father understood that their 5% essentially equaled a few hundred dollars. A suit was brought to contest the validity of the will on the grounds that the father did not fully understand the consequences of the will that he signed. During the deposition of the estate planning attorney, it was confirmed that she did not have any financial information for the father. Therefore, there was no way that she could have properly advised him on the consequences of only providing 5% to his other children. The case ultimately settled; however, had the attorney shown that she had the father’s financial information and discussed projected inheritances for his children, there would have been no case to bring. Selecting a high skilled and well respected estate planning attorney is the best defense someone can employ if there is any chance of a dispute amongst family members.”

– Marlee S. Cowan, Partner at Rubin and Rudman, LLP in Boston, MA

“I met with a client to create an estate plan and when I reviewed her assets I discovered her Ôadvisor’ had her convert most of her liquid assets to annuities. She had a taxable estate in Massachusetts and when I looked at her asset structure, it became clear that her Ôadvisor’ had sold her into products that were not in her best interest and created a huge issue for estate liquidity. She had one CD that was coming up to maturity and I suggested she seek a second opinion from a real advisor about her assets, as her current ‘advisor’ was recommending another annuity. The CD was the only money left that could be used to pay the estate tax at her death. Luckily he hadn’t taken over all of her assets and there was money to pay the tax if she passed away.”

– Kristin N.G. Dzialo, Esq., Partner at Rubin and Rudman, LLP in Boston, MA

Had Kristin’s client worked with a fee-only registered investment advisor, the situation would likely have been different. A fee-only advisor is only compensated by their clients (typically as a percentage of assets under management) and they do not sell products (like annuities) or receive commissions from 3rd parties. Only registered investment advisors have a fiduciary duty, a legal obligation to act only in their client’s best interests, which is the highest standard of care under the law.

Although few things in life are certain (death being one of them), working with a financial advisor that is both fee-only and a registered investment advisor is perhaps the best way to help ensure that your financial life is managed objectively and at the highest level. Darrow Wealth Management is a fee-only registered investment advisor.

Life and legacy: your estate plan is so much more than asset distribution

Unfortunately, a reluctance to face issues concerning your own mortality or future health possibilities ends up hurting surviving family and loved ones the most. Rather than view an estate plan as only an opportunity to avoid a negative outcome or preserve an inheritance for heirs, also consider it an occasion to outline what type of legacy you would like to leave, whether financial or otherwise.

Through the entire estate planning process, you are able to control aspects of your life and legacy that would otherwise be un-knowable, left to chance, or in the hands of an individual you may not want to decide. Aside from regular asset distribution, an estate plan can cover a wide range of concerns, from who will care for your children and with what parenting style, to medical directives and end-of-life issues, to making sure your beloved pet is provided for during its life.

As wealth advisors, we understand that the estate planning process can be overwhelming. To help support our clients through the process, we’ll work with you and your estate planning attorney to help ensure your completed plan is properly executed so nothing falls through the cracks.

Important disclosure: The material in this article is intended to provide generalized information only as to some of the estate planning considerations that have the potential to impact individuals and families and should not be misconstrued as the rendering of personalized legal or tax advice. We strongly recommend you consult an estate planning attorney in your state to discuss your personal situation and estate planning needs.