How much money do you need saved to retire comfortably? It depends entirely on how much you plan to spend. In this piece for Forbes, Darrow Wealth Advisor Kristin McKenna discusses ways investors can estimate their expenses in retirement.

How much money do you need saved to retire comfortably? It’s not a simple question to answer, but the good news is individuals sometimes overestimate how much income they will need to maintain their current standard of living in retirement. If you don’t have a handle on where your money goes now (e.g. the ‘miscellaneous’ category), it is possible that a comfortable retirement isn’t as unattainable as you think.

In general, we tackle retirement expenses in one of two ways: projecting current spending into retirement or backing into a sustainable level of annual income based on current assets and savings rate.

For either of these methods to yield useful data, it’s critical to first understand your current spending and what major costs will likely fall off in retirement.

What are you spending now?

As simple as it sounds, it’s not that easy to know where your money goes. Expenses are lumpy: perhaps you pay your homeowners insurance annually, don’t take a major trip every year, or pay quarterly tax estimates.

The slow creep of lifestyle inflation doesn’t help either. As income grows, it’s tempting (and easy) to gradually increase your spending—going out to eat more, buying a nicer car, considering cost less and less as you plan a vacation.

Some major pre-retirement expenses disappear in retirement

Retirement marks the end of a lifetime of saving for it. Pre-tax contributions are taken from your paycheck before you ever see it, so it’s easy to overlook the offset to your income. These contributions are substantial: in 2020, a couple under age 50 could save $39,000 per year in a 401(k) plan and $52,000 if 50 or older.

Here are some other expenses that often disappear in retirement:

- Payroll taxes: FICA taxes (Social Security and Medicare) currently equal 6.2% of taxable wages for the employee—the employer pays the same share. Retirees don’t have to pay FICA taxes on distributions from IRAs or a brokerage account. For business owners, the savings is double.

- Contributions to 529 plans or tuition payments: depending on your life stage, you might still be putting kids through college or saving for it down the road. Most individuals retire after their kids are through college and have become independent, so these major costs aren’t usually a retirement expense.

- Life insurance premiums: investors sometimes think they need life insurance forever, but many families do not. As kids launch their own careers and investable assets grow, the need for life insurance typically declines.

- Transportation to work: whether you’re paying for a commuter pass, parking, or wear-and-tear on a car from an extended commute, non-leisure transportation costs can add up during working years.

Forecasting retirement expenses

Adjusting your current spending to reflect a retirement lifestyle is a good place to start when trying to figure out how much income you’ll need in retirement.

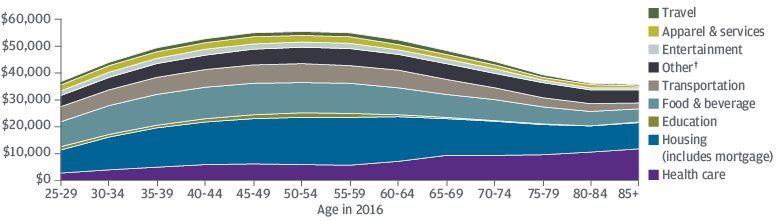

Before redlining all your major expenses, one area of spending that probably won’t go away in retirement are housing costs. As indicated by the Chase data below, the majority of retirees still pay housing costs throughout life as a major expense.

Median Household Lifestyle Spending By Age

Source: Total spending and all category sub-totals except checks, cash and health care costs: Chase data, including Chase credit card and debit card (excluding some co-branded cards), electronic payment, ATM withdrawal and check transactions from January 1–December 31, 2016; J.P. Morgan analysis.

Even if you’ve lived in your home a long time, you’ve probably refinanced along the way.

Especially in today’s low interest environment, not getting a mortgage on your retirement home could be a missed opportunity.

Managing the surge

Before getting too bogged down in how much your travel budget will be, recognize that what you choose to spend money on will change throughout retirement. As some costs increase (like healthcare), other expenses (like food and travel) will decrease.

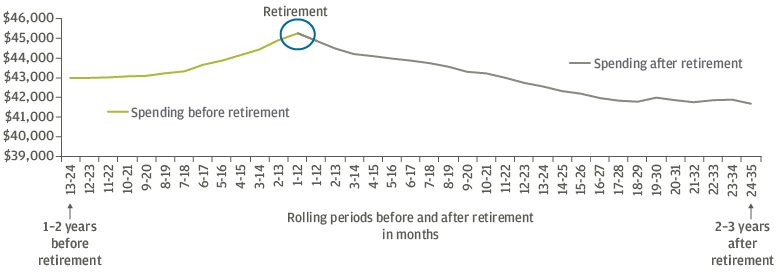

While spending will ebb and flow over the years, the period where it is most important to monitor expenses are the years just before and after you retire. This period is pivotal because retirement savings are generally at their highest levels, making you most vulnerable to stock market volatility.

Taking money out of your accounts at the beginning of retirement intensifies these risks. Unfortunately, according to data from Chase, this period also typically marks a surge in spending.

Rolling Monthly 1-Year Median Spending Before and After Retirement (Retirement age 60-69)

Source: Chase credit card, debit card (excluding some co-branded cards), electronic payment, ATM withdrawal and check transactions from October 1, 2012 to December 31, 2016.

Keeping fixed costs low and manageable helps retirees and pre-retirees navigate different economic conditions and unforeseen challenges as they are better equipped to adapt. Substantial fixed monthly costs (carrying costs of homes, vehicles, etc.) can force investors to keep tapping their accounts during bad times, leaving fewer dollars invested for the recovery.

The role of planning

Even if you have a detailed budget, it’s difficult to know what things might cost 30 years from now and how your lifestyle expenses could change in retirement without the support of an advisor.

Developing a comprehensive retirement plan can help investors work through the numerous investment, economic, and lifestyle decisions that will need to be made before and during retirement.

In particular, the affordability of healthcare in retirement, especially for early retirees, is of great concern. Fidelity’s 2019 Millionaire Outlook Study found that paying for healthcare is the biggest source of stress for investors of all means.

If you’re just getting started, first work to recalibrate your current spending for retirement to assess whether you’re on the right track given your asset level and ongoing savings. Investors within 20 years of retirement may want to consider consulting a financial advisor.

Having a long runway before retirement can make it easier for individuals to reach the retirement lifestyle they want without the need for drastic cutbacks along the way.

This article was written by Darrow Advisor Kristin McKenna and originally published by Forbes.