Early Exercisable Stock Options, Key Summary:

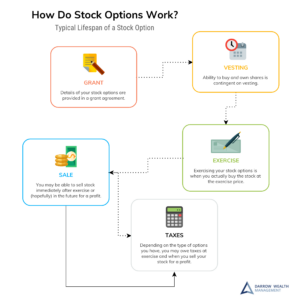

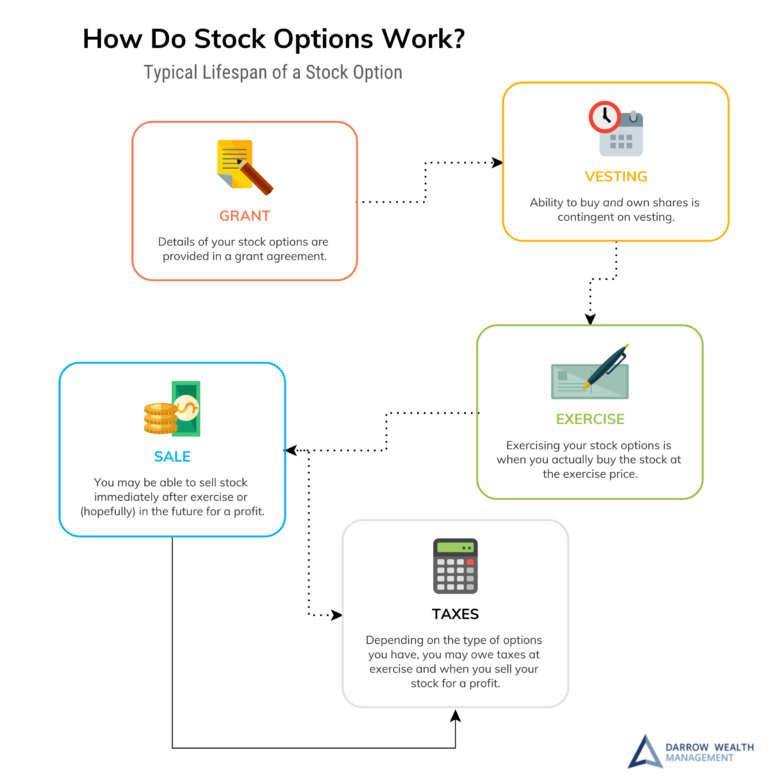

Exercising stock options means buying shares. Early exercising stock options means buying the stock before it vests. When should you exercise an option early? In the right situations, early exercising stock options can reduce tax when paired with an 83(b) election. And if you have incentive stock options (ISOs), it may be a way to avoid triggering the alternative minimum tax (AMT). An early exercise starts the holding period for long-term capital gains. For some startup employees, it could be the key to qualifying for tax-free stock sales down the road.

It doesn’t always make sense to early exercise unvested options, so it’s important to understand the risks, pitfalls, and tax implications first.

Before getting into the pros and cons of early exercises, a word of caution. Employees with stock options often focus on one thing: taxes. And specifically, how to reduce them at all costs. Don’t fall into this trap. Sometimes, exercising options early is a terrific opportunity; other times it’s a terrible idea. Before getting wooed by the glimmer of potential tax savings, understand the risks, rules, and ways this approach could backfire.

What are early exercisable stock options?

In most stock plans, option grants vest over time and exercising isn’t possible until shares are fully vested. But some companies offer employees the option of exercising early, before they have vested options, and the potential tax savings can be huge.

An early exercise of stock options doesn’t change the vesting schedule. So employees with equity compensation still need to earn their startup equity. Exercising early also won’t change your purchase price or expiration date of the company stock grant.

However, when everything goes according to plan, exercising options early has the potential to drastically reduce taxable income compared to a typical exercise.

The reason is simple: if the valuation keeps going up, so does the spread above your strike price. The larger the gap, the harder it is to exercise stock options at a private company and the more you’ll pay in tax as a result (all else equal).

This article has more on regular stock option exercises.

Recap: Tax treatment without early exercise

Understanding the potential benefits of early exercisable employee stock options requires knowledge of how stock options are taxed. In the typical scenario, there are no tax implications at grant or vesting. Below is an overview of the federal tax treatment of stock options. Your state has its own tax laws.

Incentive stock options (ISOs)

At exercise

Exercising ISOs is not a taxable event for federal tax purposes. However, it is income for the alternative minimum tax (AMT) calculation if you hold shares at the end of the calendar year. The spread between the fair market value (FMV) of the stock at exercise (typically the 409a valuation) and the strike price is income for AMT purposes. This may or may not trigger the alternative minimum tax, but the income is includable in the calculation.

At sale

When you sell, it’s a taxable event as either a qualifying or disqualifying disposition. In a qualifying disposition, you hold the stock for at least 2 years from the grant date and at least 1 year after exercise. If you meet both holding requirements, the entire spread between the sale price and the exercise price is taxed at long-term capital gains tax rates.

If you don’t meet the holding requirements, it’s a disqualifying disposition. The difference between the value of the stock at exercise and your strike price is taxable as regular income, but not subject to payroll taxes. Any subsequent gain is a capital gain depending on the holding period after exercise. Currently, short-term capital gains rates are the same as regular income.

Nonqualified stock options (NQSOs)

At exercise

Exercising nonqualified stock options is a taxable event. At exercise, the compensation element, or difference between the FMV at exercise and the strike price is part of your ordinary taxable income and subject to payroll tax.

At sale

Any subsequent gain is a capital gain depending on the holding period (either short or long-term).

Video: Early Exercising Stock Options (Examples)

Taxes on early exercisable stock options

Early exercises can offer significant tax savings in certain situations. Because the employee is buying unvested stock, the income tax treatment is different than a typical exercise of vested stock options.

A key part of the process is filing an 83(b) election.

With an 83(b) election, taxpayers accelerate the tax impact for income tax purposes or the AMT. Here’s why: at grant, the strike (purchase) price usually equals the current fair market value of the stock. If shares are immediately exercised with the filing of an 83(b) election, there may be an opportunity to have a $0 spread between the FMV and strike price.

Early exercising stock options using an 83(b) election means NSOs could reach the long-term capital gains holding period a year post-exercise. For ISOs, the special holding period must be met (2 years from grant, 1 year from early exercise), for the gain to be taxable as a long-term capital gain.

Financial Advisors Specializing in Stock Options

Should I early exercise stock options?

For ISOs, when the strategy goes according to plan, there’s an opportunity to reduce or eliminate AMT and possibly start the clock early for a qualifying disposition on shares that may not vest for several years.

For NQSOs, the opportunity is typically much better. The early exercise of non-qualified stock options has the possibility to achieve the tax benefits of ISOs with a 1-year holding period and without AMT concerns.

It may make sense to consider exercising startup shares immediately if:

- Shares currently qualify for Section 1202, qualified small business stock. In this case, if requirements are met when stock is eventually sold, the exercise date starts the holding period

- Spread between the exercise price and FMV is zero

- Company is unlikely to be acquired before desired holding period is met

- You have enough cash on hand to buy the shares and pay any tax due – without selling the stock

- You are confident about the growth of the company and the likelihood of a future IPO or liquidity event

Early exercise risks

There are several serious risks when exercising unvested shares of company stock. Here are a few to consider.

- If you leave your job with unvested shares. The company can repurchase the stock at the lesser of your strike price or the current FMV. You don’t get a refund on the tax paid.

- No liquidity event. At a private company, there’s no liquid market to sell stock. There’s no guarantee there will ever be an exit, tender offer, or secondary market for cash. Exercising options at a startup can be the easiest to do financially (low strike price = lots of potential upside) but it’s also the most unclear as to the longevity and path of the business.

- Stock price/valuations decline. Regardless of whether there’s a public market for the stock or not, the value of a company doesn’t just go up. Especially if considering an exercise before an IPO, the private valuation may be higher than what the public market thinks it’s worth. Further, your taxable spread could be very large, making an exercise-and-hold all practically impossible.

- Cash and concentration risk. Exercising options can sometimes require a significant cash outlay to buy the shares and possibly pay tax. Robbing your emergency fund or taking out a loan only increases your risk. Also consider your overall concentration and liquidity. Serial startup employees may have private shares with past companies, creating an overall situation that’s very illiquid and concentrated in a few companies.

- M&A can ruin your plans. The IRS doesn’t care why you have a disqualifying disposition or short-term capital gain. If your company is bought or acquired before your holding period is met, there may be negative tax implications. Note: unexercised ISOs can be considered cancelled options in some buyouts, triggering payroll taxes.

What’s the best exercise strategy?

In certain circumstances, like when the cash outlay (purchase price + tax) is small and manageable, early exercising can be a huge opportunity. In other situations, waiting to exercise employee stock options until there’s certainty can be a good approach. Especially if the goal is diversification, knowing the tax impact and net profit helps decision-making.

Further, after an IPO, there are often other ways to purchase the stock, such as a cashless or net exercise. Public markets offer liquidity, after the lockup expires. When considering the pros and cons of any exercise strategy, don’t let the tax tail wag the dog.

Let’s Talk About Your Equity.

If a liquidity event is on the horizon and you want an advisor in your corner for the long haul — let’s talk.

If ISOs are early exercised when the strike price is equal to the FMV of the option, and an 83(b) election is made, the spread for AMT tax purposes is $0. There are no federal tax implications at exercise. At sale, if the ISO holding period is met (2 years from grant, 1 year from early exercise), the entire spread will be taxable as a long-term capital gain.

If you don’t make an 83(b) election when exercising incentive stock options early, there are no tax implications at the time of exercise for AMT or federal tax. But when the shares vest, the spread between the strike price and fair market value at vesting is income for AMT. To meet the terms for a qualifying disposition, you’ll need to hold the shares for 1 year after the shares vest (not when you early exercised) and 2 years from the grant date.

Regardless of whether you made an 83(b) election, if the sale of ISOs is a disqualifying sale, the tax treatment is likely to be the same had you filed. Although IRS guidance isn’t 100% clear, many tax professionals agree that in the event of a disqualifying disposition of early-exercised incentive stock options, the spread between the fair market value of the stock at vesting and the strike price is ordinary income for federal tax purposes. Any subsequent gain or loss is a capital gain/loss, based on the holding period after vesting and the spread between the sale price and the FMV at vesting.

At exercise, the difference between the fair market value and the NSO strike price is taxable as ordinary income and subject to payroll tax. It begins the 1-year holding period requirements for long-term capital gains tax treatment. So if the stock vests and is sold more than a year and a day after the shares were exercised, you’ll have a long-term capital gain.

If you fail to file an 83(b) election when exercising NSOs early, there are no tax implications until the stock vests. At vesting, the spread between the exercise price and the fair market value at vesting is taxable. The capital gains holding period begins when the stock vests.

This article is for informational purposes only and not to be misinterpreted as personalized advice or a recommendation for any specific investment product, strategy, or financial decision. This article does not contain sufficient information to support a financial or investment decision. If you have questions about your personal situation, consider speaking with a financial or tax advisor.

[Last reviewed February 2026]